Variant menu: Calculations >

Financial analysis > Results

Financial analysis > Results

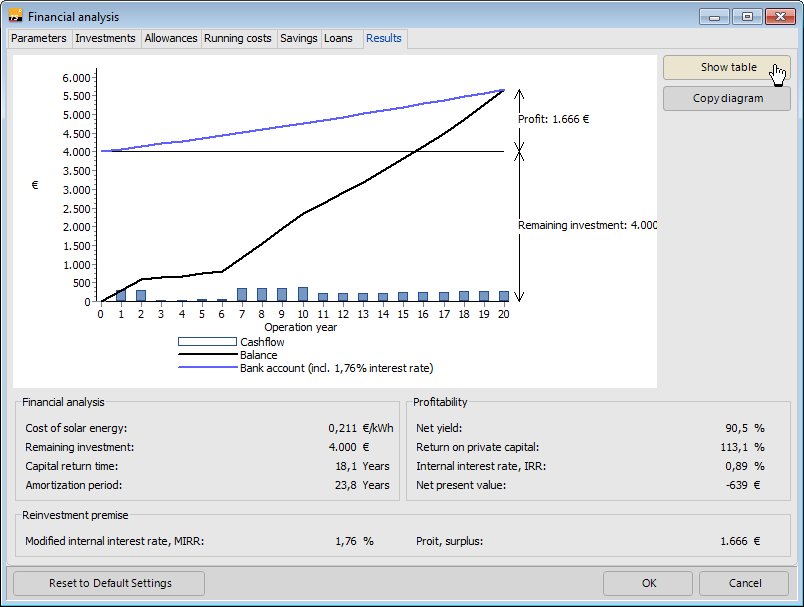

Financial analysis

The initial costs for solar (also called heating cost) is calculated with the equation: Solar production costs = total annuity / yearly solar yield

Another way goes through the capital value. If the solar yield is multiplied by the heating costs and included in the capital value in addition to the combustible fuel costs, a capital value of null is generated.

The remaining investment is calculated as: remaining investment = total investment - grants - loans and therewith corresponds to what is known as the deductible or private capital, which must be provided by the investor or client.

The capital return time is reached when the accumulated cashflows have reached the remaining investment.

The amortization period is the assumed lifespan at which the capital value will reach null. If the capital value is negative, the pay-back time is longer than the assessment period.

The following applies: Remaining investment payback time > Capital return time > Amortization period

Profitability

The Return on assets is determined with the equation: Return on assets = return on capital / (total investment - grants)

The Return on equity results from the equation: Return on equity = return on capital / remaining investment.

The internal interest rate (IRR) is the interest on capital, by which the capital value is null. With a negative internal interest rate, no positive capital value is reached. In this case, payment of the internal interest is waived. The higher the internal interest rate, the more profitable the investment. The internal interest further implies how high the loan interest can be, so that payments minimally finance the loan. An important advantage of the internal interest as a return is that it does not depend on the capital interest.

The capital value is the total cash value, which means all discounted payments over the live of the investment. Even if the capital value is negative, the investment can be profitable for the owner/user when the return on the investment is (MIRR) positive.

Reinvestment premise

The modified internal interest (MIRR) is a return, which the bank account must reach if the remaining investment is deposited in a bank account that will reach the end balance. As an owner/user, one can see this as follows. If the bank pays an interest rate (reinvestment interest, RI) that is less than the internal interest rate, the investment than earns a higher end balance. The interest rate, which the bank then must pay to reach the balance is described as a modified interest rate (MIRR):

- The IRR is therewith, a limit. If the IR is below the IRR, the investment in a solar system is more profitable. The following applies:

RI < IRR - The MIRR is the return that the solar system achieves. For an economic investment

RI < MIRRmust apply. - As a result, the following inequality must apply:

RI < MIRR <= IRR

For the investor and owner/user, the following, different limits are apply:

- The investor compares the alternatives, therefore

RI < IRRmust apply. - For the owner/saver however, MIRR is more important, since it produces the following return:

RI < MIRR. Therefore withIRR < RI < MIRR, the investment in a solar system is also interesting. Also here, if the capital value is negative, the solar system earns a higher yield than the virtual bank account.

Example

In this example, see the following effects:

- The system should run for 20 years.

- At the end of the lifespan, a bank account with the same end balance would have earned a return of 1.76% (= MIRR).

- The loan is repaid in the operating years 3 to 6 and could result in a very small or negative cash flow during these years. The loan has 2 payment-free grace periods. The balance itself cannot be negative, since the repayment must be generated from the savings already earned. If this is not the case, additional capital is required. However, a small loan is therefore taken out at the beginning.

- In this example, the remuneration ends after 10 years, which can be seen by the dip in the balance and the low cashflows.

Remaining investment payback time = 15.8 years,Capital return time = 18.1 years,Amortization period = 23.8 years- This investment is not advantageous for the investor, as the return (1.76%) is below the assumed capital interest (here 2.5%). The capital value is therefore negative and the pay-back time is longer than the lifespan.

- For users/owners, the investment is still of interest since they get hot water and a return; however small.

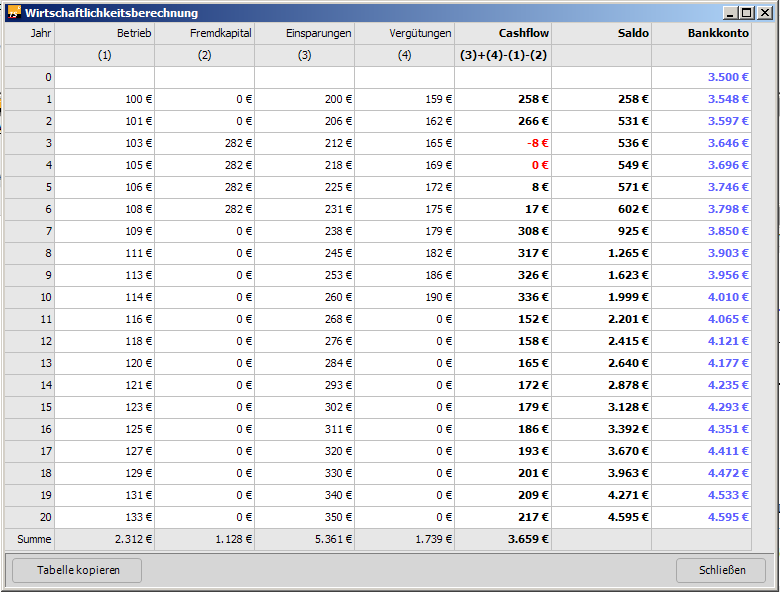

Table

In the table, the annual values are listed that form the basis for further calculations.

- The operating costs increase with the rate of the price increase and are listed in the table.

- Repayment and interest are listed in the column Loan capital.

- The Savings are determined with the special combustible fuel costs.

- Remuneration refers to the subsidies for solar generated heat.

- Cashflow is the (non-discounted) sum of columns (1) to (4), whereby the operating and loan capital costs reduce the cashflow. The sum of all cashflows (see total line) is described as a return on capital and goes into the return on equity and loan capital yield.

- If the yearly surpluses (cashflows) are invested with the reinvestment interest rate, the outcome is the indicated balances.

- The column Bank account shows that the remaining investment was alternatively deposited in an account. The achieved yield corresponds to the calculated modified internal interest rate (MIRR).