Economic parameters

General parameters

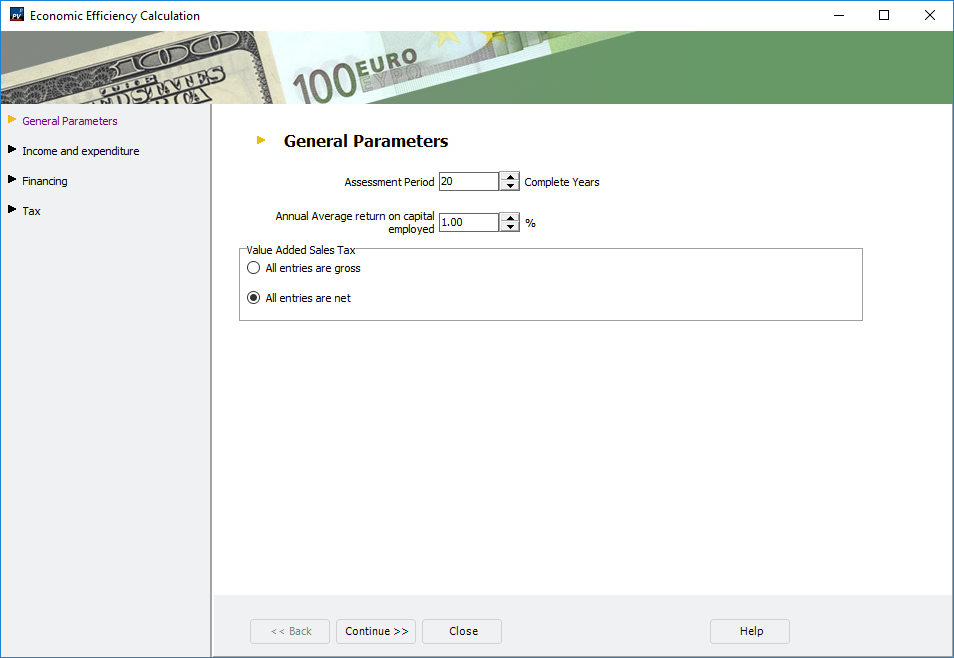

Parameters for economic efficiency - General parameters

| Parameters | Description |

|---|---|

| Review period | Full years without the year of commissioning must be stated as the period under consideration. According to VDI 6025, the period under consideration corresponds to the time span of the planning approach for calculating the economic efficiency time (planning horizon). |

| Interest on capital | The current value of the current yield can be specified as the return on capital. The current yield is the average yield of bonds. The Deutsche Bundesbank calculates these as the average value of the fixed-interest securities in circulation. The umlaut yield is thus a measure of the interest rate level on the bond market. |

| Sales tax | This input field has no influence on the calculation, but is intended to make it clear that all entries must be entered with or without sales tax. As a rule, you enter all amounts net. If you enter gross amounts, you must enter gross amounts everywhere. |

Cost balance

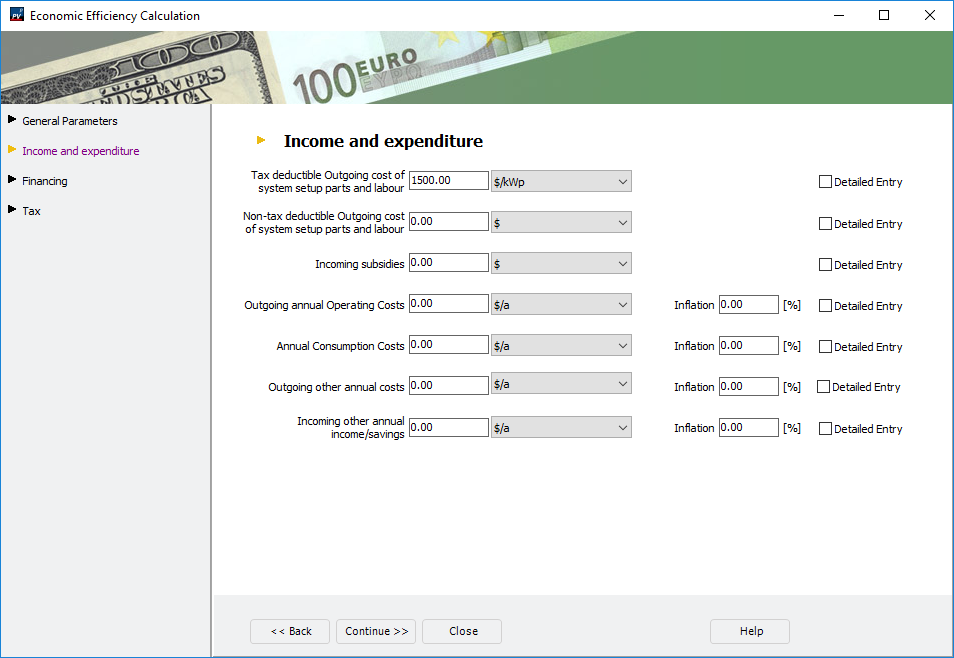

Parameters for economic efficiency - Cost balance

The feed-in tariff in the first year is calculated from the feed-in tariff and the yield resulting from the simulation.

| Parameters | Description |

|---|---|

| Depreciable investments | Depreciable investments are the total (net) acquisition costs of the PV system (material, scaffolding, assembly, etc.) required to build the system. Detailed input: Useful life The useful life is the period of economic use of the investment object in years. Useful life < Period under consideration The investment must be re-procured. The price for the replacement depends on the specified price change factor. Useful life > Period under consideration At the end of the observation period, the investment still has a residual value, which is included in the calculation of the capital value. |

| One-time payments | One-off payments are costs that cannot be written off. They are taxed directly. |

| Funding | Funding reduces costs. They do not influence depreciation, but are taxed directly. |

| Operating costs per year | |

| Consumption costs per year | |

| Other costs per year | |

| Other revenues / Savings per year |

|

| Price change coefficient | The price change coefficient indicates the average percentage change in a payment compared to the previous year. |

Financing

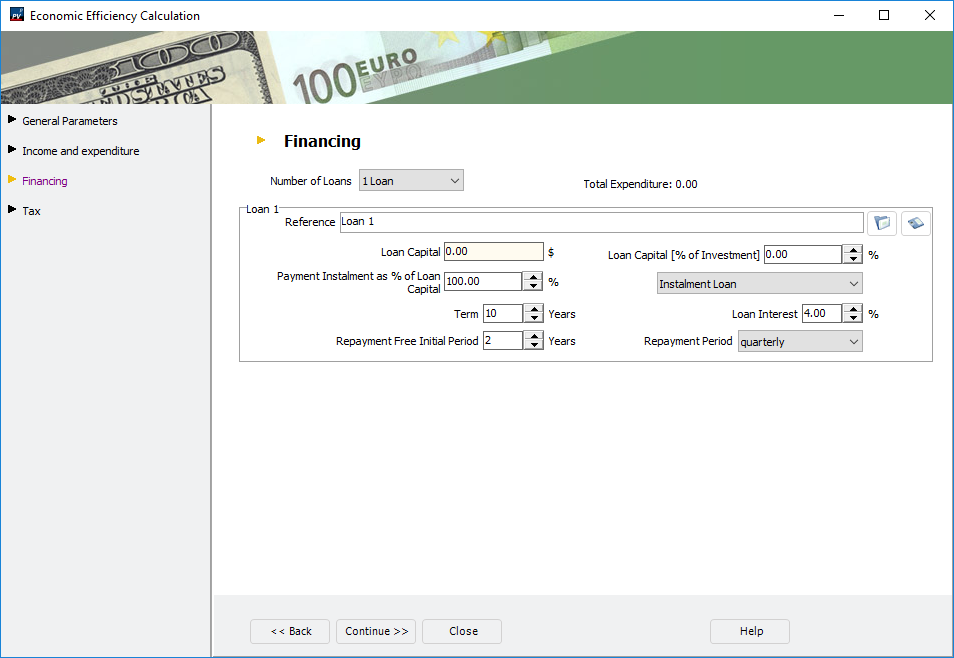

Parameters for economic efficiency - financing

On the Financing page you can define loans that are used to finance the PV system.

| Parameters | Description |

|---|---|

| Loan capital | Loan amount on the basis of which interest and repayment are calculated. The loan amount can be stated in absolute terms in euros or as a percentage of the investment volume. The investment volume here is defined as investments and one-off payments less subsidies. |

| Payout rate in % of debt capital (discount) | This value indicates which percentage of the specified debt capital is actually paid out. Please note that a discount in the results evaluation is regarded as an interest payment in the first year. The amount paid out on the loan is calculated by multiplying borrowed capital by the payout rate. The sum of the disbursement amounts of all loans should not exceed the investment volume defined above. |

| Loan period | The period after which the loan is repaid. |

| Loan interest | Nominal interest rate to be paid on the remaining debt. |

| Redemption-free start-up years | No repayment is made in this period, only interest payments. In the remaining time until the end of the term, the borrowed capital is then repaid in instalments. |

| Repayment period | Interest and instalment payments are made at these intervals. |

| Instalment loan | Instalment loans are repaid in constant instalments. The interest payments to be made are recalculated from the remaining debt after each instalment payment. The total repayment installment results from a constant repayment portion and a decreasing interest portion. |

| Annuity loan | Annuity loans are repaid in constant instalments over the term of the loan. The repayment portion within this repayment installment increases with the number of installments, while the interest portion decreases accordingly. |

Taxes

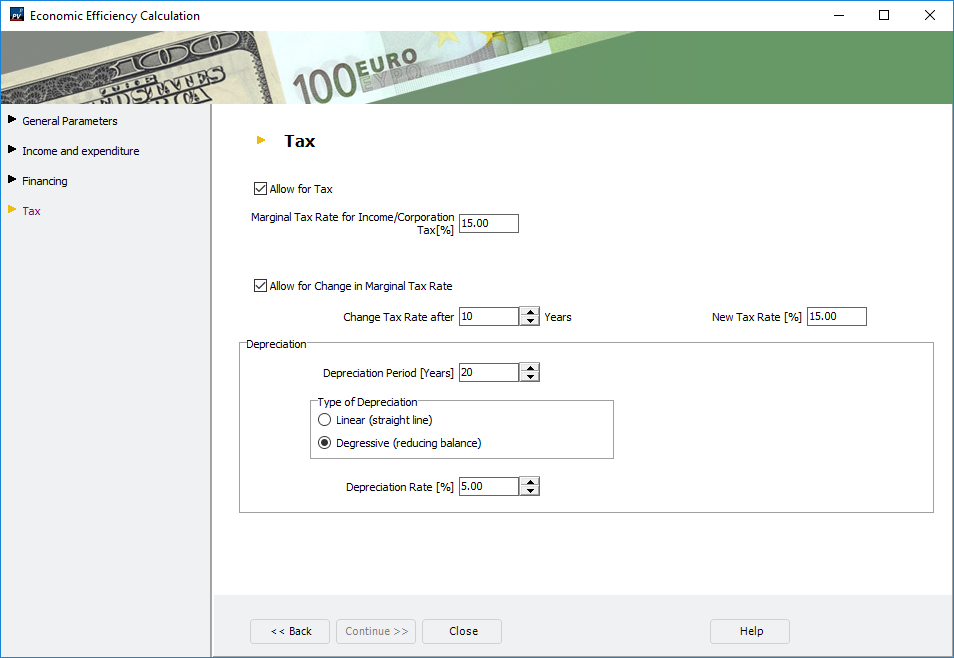

Parameters for economic efficiency - Taxes

To ensure that tax payments are taken into account in the cost efficiency analysis, proceed as follows:

-

Activate the check box

Consider taxes and Income / corporation marginal tax rate.

Consider taxes and Income / corporation marginal tax rate.This is the tax rate to be paid for each additional taxable euro (or other currency).

-

(optional)

Take into account a change in the marginal tax rate- Indication of the time of change of a tax rate

- Indication of the New Tax Rate

-

Make specifications for depreciation

- Specification of depreciation period

This is the period over which the investment is depreciated. The usual period for PV systems is 20 years. - Information on type of depreciation

- Linear

Depreciation per year is calculated on a straight-line basis by dividing investment by depreciation period. - Degressive

The annual depreciation amount is reduced above the depreciation rate. This reduces annual depreciation. If the annual depreciation falls below the value resulting from straight-line depreciation, the residual value is depreciated on a straight-line basis over the remaining period.

- Linear

- Specification of depreciation period

See also